Orlando Bravo was quick to see the disruptive potential of software, making a series of lucrative bets on the sector that turned him into a billionaire and transformed the buyout shop he leads, Thoma Bravo, into an industry powerhouse. Now, the disruption is coming for his own firm.

The Miami-based financier is confronting it head-on, seeking to ensure his empire is ready for the era of artificial intelligence — and reassure investors that a debt-laden bet on online customer surveys, which lost more than $5 billion, is a one-off. The fund that held the investment is lagging behind rivals, and investors are on high alert for other potentially stressed deals.

The challenges illustrate two big questions facing private markets: How can software companies sustain the high margins and stable cash flows that made them investor favorites, if AI models can replace coders? And what happens to the many richly valued takeovers done earlier this decade when borrowing costs were at rock bottom?

Thoma Bravo’s losses on the customer-survey firm, Medallia Inc., stirred up concerns over its concentration in software — a “sector that’s going to go through some very rough times,” said Gustavo Schwed, a professor at NYU Stern School of Business.

Given Thoma Bravo’s strong track record, a single large writeoff “is not dispositive,” said Schwed, a former private equity investor. “The bigger concern is: How many more of these are there?”

Investors appear to have the same question. Some private credit lenders are pulling back from financing Thoma Bravo’s companies, while buyers in the market for second-hand fund stakes have started shying away from deals that include Thoma Bravo and its tech-focused peers, according to investors in the market. Would-be buyers have concerns that investments in the funds may not be worth what the buyout firms paid for them,and are commanding steeper discounts to acquire their holdings.

Then AI took off. Earlier this year, Anthropic PBC rattled investors by releasing new tools to automate tasks in areas such as legal services. Thoma Bravo and other software investors rushed to assure clients that their portfolios were healthy.

For software providers, a big risk is that corporate customers drop specialized products and instead use AI models to sift data, handle workflows and generate reports — or even use tools like Anthropic’s Claude Code to “vibe code” their own bespoke apps.

Read more: What’s Behind the ‘SaaSpocalypse’ Plunge in Software Stocks

Even for software companies that embrace AI, new revenue models are required, since the hefty computing costs of responding to queries changes the industry’s economics, according to the consultancy firm Bain & Co.

Software heavyweights like Thoma Bravo, Vista Equity Partners and HG Capital are investing heavily in response, said Hugh MacArthur, Bain’s global chairman of private equity. These investors are running pilots on incorporating AI and creating new products, knowing not all businesses will succeed, he said. He ultimately expects the buyout firms to succeed.

“They’re aware this is an existential issue for them: This is not optional,” said MacArthur.

In Thoma Bravo’s case, its recent funds have acquired nearly 30 AI-focused companies since mid-2023, representing nearly $3.5 billion in enterprise value, according to a recent letter to investors. Its portfolio expects to generate about $5.2 billion in AI revenues this year, the letter said.

In addition, portfolio companies have ditched less-certain projects to focus on initiatives with a “justifiable” return on investment, while firm executives are encouraging the businesses to adopt AI faster, Bravo said in the same interview.

Thoma Bravo is deepening links to Alphabet Inc. through the multiyear Google deal, which followed a fact-finding trip by portfolio company bosses to Silicon Valley, Bravo said.

The firm has also tightened its focus by ending a disappointing foray into investing via smaller, “growth equity” stakes. Its sole growth fund, dating from 2021, is a fourth-quartile performer with a negative return, Bloomberg data shows.

Loan Bargains

At the same time, Bravo and his colleagues are talking up potential opportunities. Bravo says fears of a so-called SaaSpocalypse have faded away, as investors come to see that these businesses can adapt to incorporate AI.

“It is finished. No more. It’s pretty simple. People are realizing that these are unbelievable companies,” he told Bloomberg TV in an interview at this year’s SuperReturn conference in Berlin.

He stresses how Thoma Bravo-backed companies like Coupa Software Inc. are evolving, for instance, by developing their own “small-language models” to grow and stay competitive. These models focus on specific tasks and use fewer resources than more general large-language models.

The firm sees enterprise software offerings with strong data and customer “moats” as best placed to withstand the AI threat. Executives highlight Jeppesen ForeFlight, a digital-aviation business bought from Boeing Co. last year for $10.6 billion, and Dayforce Inc., a payroll, employee records and benefits company it acquired earlier this year, as two strong examples of this. Thoma Bravo executives contend that rising digital security threats could benefit cybersecurity firms.

Bravo has extolled an unparalleled “opportunity to automate human judgment” that will favor well-run companies with domain leadership and decades of experience. Speaking in May at the Milken Institute Global Conference, a major Wall Street confab, executives discussed the firm’s relationships with the biggest providers of AI models and said they were hunting for bargain software loans.

And at a March investor meeting, portfolio companies set up booths to show how they are using AI. Thoma Bravo has also hosted investor webinars about how it is responding to the AI threat, people with knowledge of the matter said.

But some of Thoma Bravo’s challenges predate the widespread use of AI models such as ChatGPT and Claude.

‘Way Overestimated’

“On a scale of 1-10, how likely are you to recommend our brand?”

Today it can feel like every hotel stay, car rental or cellphone upgrade is followed by a request for feedback. Medallia has played a role in this boom, helping well-known brands such as Airbnb Inc. and Johnson & Johnson gauge customer and employee sentiment.

Chicago-based Thoma Bravo led a $6.4 billion buyout of Medallia in 2021, while ultralow interest rates were fueling a dealmaking boom. Executives touted a “best-in-class” software business where AI could help drive growth.

Financing came from a $17.8 billion fund Bravo’s firm had raised the previous year, alongside outside investors including Abu Dhabi’s Mubadala Investment Co., and nearly $2 billion of debt from a group of private lenders led by Blackstone Inc.

The debt was riskier than a typical public bond or loan deal, because Medallia’s ability to borrow wasn’t judged by traditional proxies of the cash it could generate, but by a looser measure tied to so-called recurring revenue. Lenders also allowed Medallia to defer cash interest payments — a setup known as payment in kind that can help a debtor conserve cash but that can lead to future trouble.

The debt, which grew to nearly $3 billion in the following years, proved unsustainable, as Medallia confronted fierce competition and multiple management changes. In spite of achieving double-digit revenue growth, the consumer-research company struggled to generate enough cash to service its debt as it spent aggressively to compete with rivals such as Qualtrics International Inc.

Thoma Bravo has now lost its entire $2.5 billion equity investment, after refusing to inject more capital.Co-investors have lost roughly the same amount. It’s among among the biggest wipeouts for any private equity deal done since the global financial crisis.

The lender group, which also includes Apollo Global Management Inc. and a partnership between Future Standard and KKR & Co., is now taking control in what will likely be one of the biggest debt-for-equity swaps in private credit history. Major creditors have already written down the value of their loans by 40% or more, according to regulatory filings, implying combined paper losses of more than $1 billion.

For Bravo, the diagnosis is straightforward. “We way overestimated or extrapolated the very high rate of growth,” he told CNBC in March. “We made a mistake. And that caused us to pay too much.”

Market Reset

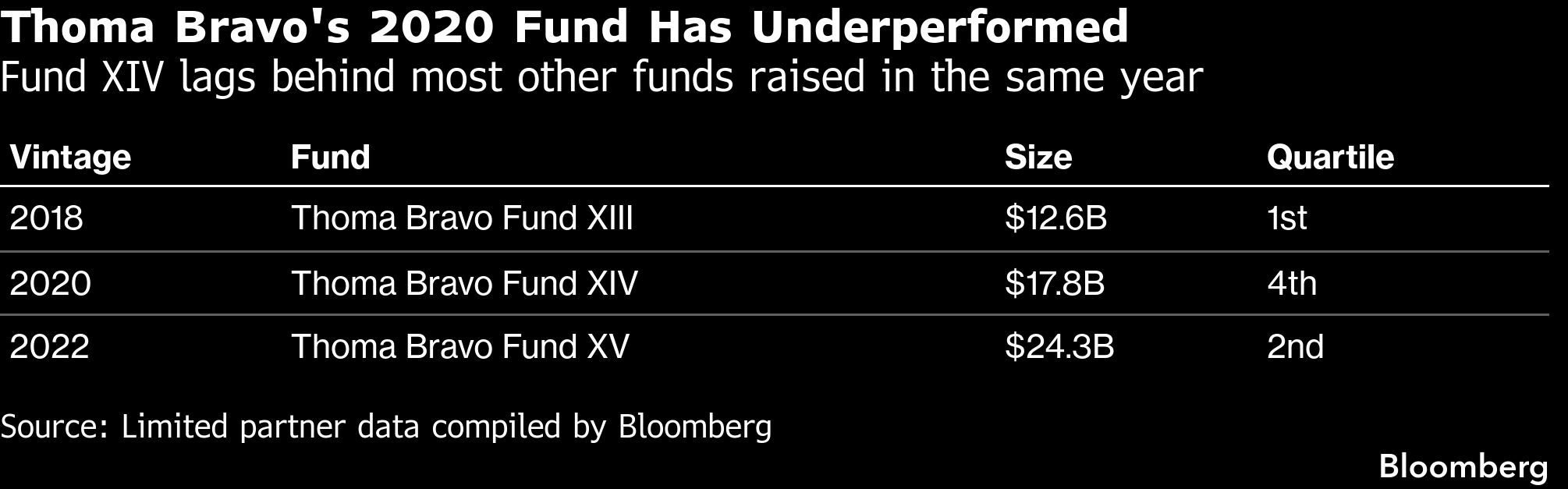

The troubles at Medallia have weighed on the firm’s 2020 vehicle, Thoma Bravo Fund XIV.

Annualized performance, based on an industry measure known as net internal rate of return, stands at just 5.8%, data compiled by Bloomberg shows, undershooting at least three-quarters of similar funds. So far it has returned just $0.32 for every dollar of cash paid in by investors.

Bravo says Medallia’s issues are idiosyncratic. And aperson close to the firm says the fund has had some early successes, including the sale of Adenza Group Inc., which generated a $1.4 windfall for the firm.

But investors are watching some of its other portfolio companies with private credit funding, given concerns about AI vulnerability. Several private credit firms recently snubbed a $2.5 billion refinancing for the cybersecurity firm Sophos, in spite of a steep increase in yield, Bloomberg reported in May. Some lenders that previously worked with Thoma Bravo declined to participate because their appetite for software deals has shrunk, according to people with knowledge of the matter.

In total, Thoma Bravo funded at least a dozen leveraged buyout, or LBO, deals between 2021 and 2025 with private credit loans, some of which were obtained based on recurring revenue rather than traditional earnings metrics,according to data compiled by Bloomberg. Concerns about software exposure, plus a wave of redemptions from small investors, have sparked a difficult reset in the nearly $2 trillion private credit market.

That could make it harder and more expensive to raise this kind of capital in the future. Lower valuation multiples for software companies could also complicate refinancing efforts as lenders typically strive to keep debt loads below 30% of a company’s total value.

“There is a pipeline of defaults that are already baked into the system from what I would call the LBO bubble of 2021,” Holly Kim, founding partner at Glendon Capital Management, told the Bloomberg Global Credit Forum this month. Many companies will struggle to refinance their share of some $500 billion of debt that is coming due in the next couple of years, she said.

Dry Powder

This isn’t the first setback Bravo has faced. While his debut software investment in the early 2000s was a home run, a spate of bad deals soon afterward nearly derailed his career, he has said.

More recently, Thoma Bravo has weathered challenges including the global financial crisis and the economic dislocation sparked by President Donald Trump’s trade war. In the 2022 “crypto winter,” it took a $130 million hit on the failed cryptocurrency exchange FTX Trading Ltd.

Some investors, or limited partners, point to Thoma Bravo’s strength in operating companies, and the senior team around Bravo. They highlight leaders such as Holden Spaht, the managing partner in charge of the firm’s application software strategy; Seth Boro, another managing partner who focuses on infrastructure and cybersecurity; and A.J. Rohde, a senior partner who manages middle-market investments and is known as the firm’s “Mr. Fix It.”

Between 2021 and 2025, Thoma Bravo’s private equity funds have generated $52 billion in liquidity, according to a person familiar with the matter.

Another valuable asset: tens of billions of dollars that the firm has raised but has yet to spend. This dry powder includes the majority of a mammoth $24.3 billion fund raised in 2024. That spares Bravo and his team from trying to gather new money in the current uncertain environment — and buys time for them to show progress on AI before hitting the fundraising trail again.

“You have to be part of the future,” Bravo told Bloomberg at the conference in Berlin. “But you have to stick with what you know really well.”

Davide Scigliuzzo of Bloomberg contributed to this report.

Top photo: Orlando BravoPhotographer: Scott McIntyre/Bloomberg

Copyright 2026 Bloomberg.